Over the past few years, a common chorus has been that fundamentals just don’t matter in this current market environment. It is all about the macro, the Fed’s balance sheet, liquidity, money flows, and performance chasing. We would agree with this assessment; fundamentals have taken a back seat to big macro. But now, with yields rising and liquidity being pulled back, fundamentals may start to matter more.

The good news is fundamentals for the equity markets are actually looking pretty good. We have just about completed the Q4 earnings season, and it was once again another great season – with over 80% of companies reporting, 78% beat earnings estimates and 70% beat top-line sales forecasts. Relative to Q4 2020, earnings are up a whopping 28%, and sales are up 16%. That is fantastic growth and evidence that while costs are rising, top-line revenue growth is helping offset them. Companies are essentially passing on higher costs to the end consumer, in case you hadn’t noticed.

Operating margins for the S&P 500 are higher than at any point over the past thirty years, as is sales growth. Because of the operating leverage within most

companies, there is a solid relationship between sales growth and margins. Sales growth is benefiting not just from good economic activity but inflation. Margin improvement has been rather pervasive, with 10 of 11 sectors enjoying improving margins in 2021. The one exception was utilities.

The TSX is enjoying similar trends of late, with strong earnings and sales growth with good margins. The fact is, 2021 was a stellar year for North American equities. As we have highlighted a few times, this was partly due to the pandemic changing consumers and companies' behaviours.

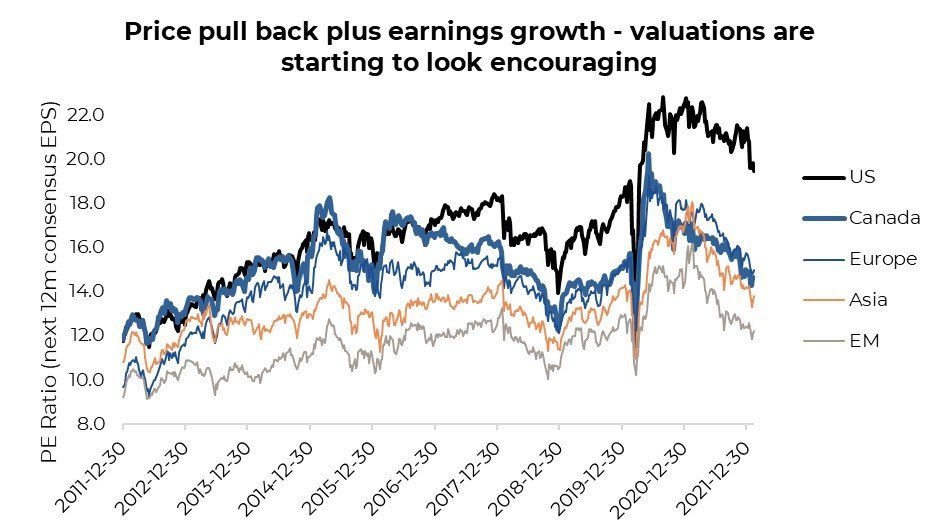

Valuations provide more good news –

if you combine the varying pullback in markets since the start of 2022 with the strong earnings growth, valuations are actually getting interesting. The S&P 500 is now trading just under 20x, its lowest since coming out of the pandemic induced bear market. Canada is below 15x, which is below its long-term average. Looking at Europe, Asia, and Emerging Markets (EM), the valuation froth is no longer an issue.

But where does the buck go next?

One reason valuations have likely come back down is that the outlook for earnings growth is starting to losepace. U.S. GDP is forecast to slow from 5.7% in 2021 to 3.7% this year and 2.5% next year. As a result, inflation is forecast to slow as well. Combine those with costs that are still likely rising, and you can imagine these record-high margins may be at serious risk of coming back down fast.

To give you an idea how fast this may decelerate, S&P operating earnings grew by over 60% in 2021. Sure, that was compared with 2020, but this growth is forecast to slow down to 9% in 2022. And that deceleration hits in Q1.

Investment Implications

This year has a lot of significant macro events going on. Going back to the office appears to be one; central banks changing direction on stimulus is another. However, slowing growth does not seem to garner much attention. While not negative growth, slowing growth along with stimulus removal makes for a more challenging market. Mark my words: it won’t be long before people start talking about a ‘hard or soft landing.’

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only.

This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used herein under a non-exclusive license by Echelon Wealth Partners Inc. (“Echelon”) for information purposes only. The statements and statistics contained herein are based on material believed to be reliable but there is no guarantee they are accurate or complete. Particular investments or trading strategies should be evaluated relative to each individual's objectives in consultation with their Echelon representative.

Echelon Wealth Partners Ltd.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Ltd. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.