The bear market in global equities is now in its 11th month, not necessarily long for a bear market but indeed approaching the average duration.

Then again, global bonds are in their 23rd month of a bear market. Noteworthy that each asset class peaked in January, equities in January of this year, and bonds in January 2021. Naturally, and with 20/20 hindsight, when global bonds yielded 0.82% in January of ’21, the risk vs reward was certainly tilted pretty heavily towards risk. Now that the value of global bonds has contracted by a mind-blowing $130 trillion (USD) and yielding 3.8%, the risk/reward does appear tilted the other way. Equities (aka stock market) are a bit more complicated.

At their peak in January of this year, global equities had risen about $30 trillion from BEFORE the pandemic.

That has all been given back, and now the market is trading a more reasonable 14x. But not sure the equity risk/reward probabilities are tilted in either direction.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used herein under a non- exclusive license by Echelon Wealth Partners Inc. (“Echelon”) for information purposes only. The statements and statistics contained herein are based on material believed to be reliable but there is no guarantee they are accurate or complete. Particular investments or trading strategies should be evaluated relative to each individual's objectives in consultation with their Echelon representative.

When attempting to gauge the risk/reward trade-off, it is all about probabilities and magnitude. Let’s talk bonds first. There is a probability or chance that six months or a year from now, inflation will remain a problem and bonds have had to yield more to compensate investors (prices go down further). Perhaps wages spiral, or there is a policy mistake, or the economy takes off. Possible. But more likely, in our opinion, is inflation begins its long road back in the downward direction as behaviours are returning to normal, supply issues are being resolved, and the global economy is slowing. Forgot one, the stimulus (fiscal cheques, near 0% central bank rates & quantitative easing) that was all turned-on full bore in 2020-21, and this has a lagged impact on inflation, which was clearly felt in 2022. This year, no more cheques, a rapid rise in central bank rates, and quantitative tightening. If the lagged impact works both ways, inflation will come down.

With that inflation view, the bond outlook is tilted more towards reward than risk. Having the probabilities in your favour is important, but so is magnitude. How much can you expect to gain if you are right, and conversely, how much could you lose if wrong. For this, the current price becomes very important, and obviously, where the price could go.

If yields rise by another full 1%, the global bond market will drop about 6.7% based on its current duration. But with a yield of 3.8%, a good chunk of this decline would be offset (of course, depending on the speed, given the yield is an annual number). Note that this offset was seriously missing when yields were below 1%. The longer this bond bear market goes, the less potential downside it has left.

On the positive side, if inflation comes down as the global economy flirts with a recession, bond prices should rise. And that current yield will still be a positive boost. A double-digit return in bonds may be in the cards, with the timing of the start very uncertain.

Equities – Two roads

There is always uncertainty about the future path of markets, and today the paths forward for equities remain very divergent. The good news is with the global equity bear market in its 11th month and down -25%, this bear is getting up there in both drop and duration. Bears don’t die of old age, but this is no cub. We believe there are two most likely paths forward from here:

The good road: Often, when the root cause of a bear market begins to improve, the bear market ends. That means inflation has to start improving, which may be getting close. The October data (out Nov 10) for the U.S. has a number of base effects that should bring down the headline number…or not. It is clearly stickier than most thought, including ourselves. When inflation does begin to improve, this could mark the end of the bear even without a capitulation event and with a potential recession on the horizon. Depending on the tenor of the economic slowdown, this would alleviate inflation pressures – so one negative (recession) and one positive (less inflation), which is bigger, is the tough question.

A rollover in U.S. inflation coinciding with a seasonally strong period for markets, given everyone is bearish, makes a Santa Claus rally a distinct possibility.

The bad road:

Something could break in the meantime. There are a lot of stresses in the market due to the rapid rise in rates & yields. Add to this high food and energy prices while the U.S. dollar rose materially and quickly. This is putting pressure on many economies and many financial mechanisms. There have been some cracks, but markets have absorbed all these big changes so far. Are there emerging markets near the breaking point due to dollar strength and food/energy costs? So far, markets remain orderly; lower, yes, but orderly. Should these stresses trigger an event, it would likely be the missing capitulation this bear has thus far avoided. And likely be the bottom.

From a probability perspective, we do believe either of these roads is very plausible. We are a bit more inclined towards the ‘good road’ but not convincingly so. Plus, there are obviously other potential roads.

The only thing we can say with greater certainty is volatility is not going away anytime soon.

There is simply too much going on.

This brings up magnitude, which has to incorporate price or where markets are today. On an

encouraging note, high inflation, central bank hawkish responses, recession risk with slowing economic growth and the need for earnings estimates to come down are all well-known by the market. And at least partially priced in.

The next few quarters will likely remain volatile in both directions. Fortunately, entry points today in either equities or bonds do offer a compelling 12-month outlook. In a year, inflation will likely have subsided to a degree. If a recession arises in North America, it should be largely played out by that point. There might be better entry points ahead, but one-year return expectations are the best we have seen in many years, given current yields and valuation. It is based on this view that we remain comfortable with being market-weight equities and bonds. Should either market sell off more, it would be more enticing to go overweight at that time.

Leaning into the yield factor

The future direction of inflation and global bond yields is one of the largest factors in determining when the bear markets in bonds and equities will end. With U.S. 10-year yields above 4%, and the Fed issuing yet another super-size rate hike, bond market volatility has actually begun to fall from the highs of early October. Perhaps we’re nearing peak hawkishness for central banks. Globally, dovish central bank surprises have recently outnumbered hawkish ones. By no means does this mean that short-term rates have peaked, but the path of hiking is beginning to slow. For example, the recent dovish surprise from the Bank of Canada and Australia are hints of this shift. These two countries are more sensitive to slowing global economic growth. The Fed is the elephant in the room of course, yet even Jerome Powell hinted at a change in cadence at future meetings. A pivot to slower rate hikes would require inflation to cooperate, but we’re seeing some signs of this as well. It’s still too early to see if this will result in a lower terminal rate.

After the quickest pace of monetary tightening since 1981, the chart above shows market expectations for the federal funds rate over 2023. The current terminal rate is 5.17%. About

63bps higher and a couple of months later than the market was expecting at the end of the third quarter. The uptick in bond yields and hike expectations has been a common occurrence over the course of 2022, but what should stand out is how quickly the ramp-up in rates will flatline. If this were an Avengers movie, we might not be in the Endgame yet, but more like

Infinity War, the beginning of the end…hopefully without the blip.

Fixed Income – Taking one more step up in duration

As rates move higher, it has been our strategy to shift away from short-duration bonds slowly while incrementally adding duration in stages, as we are never going to be able to market time-peak rates. Across our multi-asset portfolios, we’ve increased duration back to approximately 5.0. Still shorter than the Canadian market duration of 7.3 years but closer to neutral. As noted in the previous section, the increase in yields has provided a larger buffer for fixed-income investors against interest rate risk. In investing, how much you pay for an asset is a key factor to the potential downside risk. Bonds have been beaten down, and what you are currently paying means the magnitude to the downside is just less. Thanks to the cushion, higher coupon payments provide. Any hint of a real recession or a sniff of anything mildly dovish in nature from the Fed, and we could witness an abrupt turnaround into a rally in bonds.

Equities – Rate sensitives look appealing

Increasing duration isn’t the only portfolio move we’ve initiated recently. The belief that we’re nearing peak yields has us focusing much more on the yield factor within dividend-paying equities. This tilt prioritizes companies that pay higher dividends but also incorporates dividend sustainability and quality. As a bonus, it’s a defensive factor meaning that it tends to benefit during periods of economic contraction. With a recession potentially on the horizon, we are wary of having too much cyclical exposure.

We’ve written previously about the spectrum of dividends, which you can see on the chart to the right. Given our view that we’re nearing peak hawkishness, this sizeable headwind should subside, benefiting rate-sensitive sectors. One of the most rate-sensitive sectors is Utilities. Historically low beta, mature companies with durable demand that can weather difficult economic environments. Regulated Utilities also have a decent amount of pricing power to handle high inflation environment by passing along cost increases. Valuations have improved recently as the sector sold off significantly over the past few months, making valuations and the dividend yield even more attractive.

Utility stocks are historically one of the more rate-sensitive sectors and are significantly impacted by changes in interest rates for two main reasons. They are highly levered and are often viewed as bond proxies meaning that they are often viewed as a close equity substitute to bonds.

The Canadian Utilities sector yields 4.5%, with many companies yielding north of 5%.

Recent selling intensified in September and October on the latest uptick in bond yields. The sector is now barely outperforming the broader market in 2022, having lost nearly 15% relative to the TSX over the past few months as seen in the chart below.

Much like our strategy to increase duration, tilting towards the yield factor is a process. Within the Purpose Core Equity Income fund, we have recently moved to market-weight Utilities after a long period of being materially underweight. The timing is right, with a disinflationary phase on the horizon. At present, we continue to have some concerns that a challenging macro backdrop will continue to pressure more cyclical sectors. With bond yields likely to be capped near-term, the outlook for more rate-sensitive securities with a high yield factor looks promising, and we have been buyers.

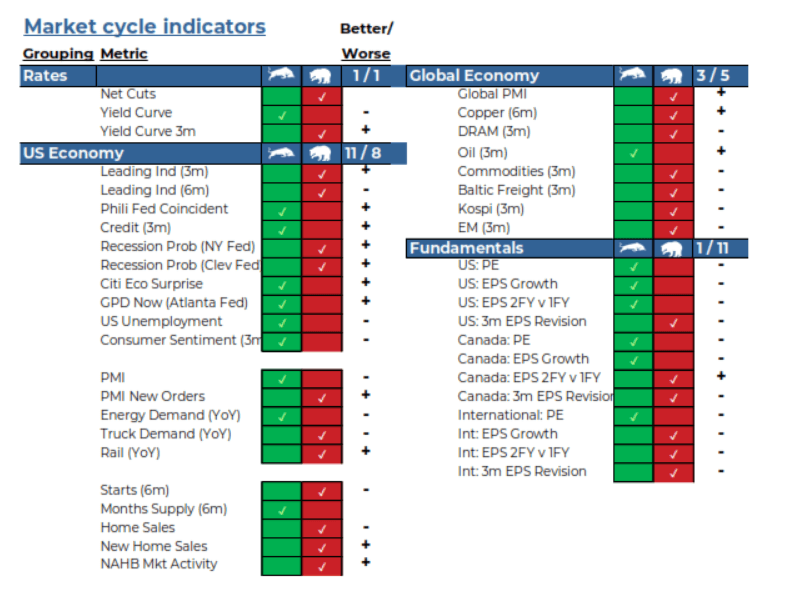

Market Cycle – stable for now

The global economy is slowing, with evidence supporting this view rather pervasive. Honestly, though, this has to be the most talked about recession ever. Usually, they surprise at least a few market participants. And while a recession or economic slowdown is not a good thing, below we have outlined why it may not be all that bad:

- Inflation concerns remain a bigger angst for the markets and have been the primary reason that equity and bond markets are down in bear market territory. Slowing economic growth or even a recession would alleviate much of the inflation pressures – not all of it, given a few lingering supply issues and the war, but much of the pressure. The market lift from falling inflation concerns may even be bigger than the headwind of a recession, especially given markets are already down a hefty amount.

- There is also the desynchronized nature of the economic slowing. The recession in 2008/09 was terrible, and what made it worse was the fact that pretty much all economies around the world went into recession at the same time. We all went over the falls simultaneously. Today, we have a material slowdown in China and Europe. Canada is doing well but slowing fast. America, they are doing a bit better than well and just starting to show signs of slowing. By the time a slowdown or recession hits North America, China or Europe may be already coming out the other side. If/when China alleviates their zero covid policy, there will be a good amount of pent-up activity. This desynchronized nature should mute the market impact of a slowdown. Of course, there is the risk of things synching up. Time will tell.

- The consumer is healthy. Maybe not as much in Canada with our household financial leverage, but the U.S. and European consumers are in good shape, and they matter much more. This has the potential to soften the impact of slowing economic growth.

- Goods-to-service spending was going to trigger a slowdown. If you spend a dollar on goods, it has a bigger impact on the economy and corporate earnings compared with a dollar spent on services. Societies pivoted to more goods spending during the pandemic supercharged the economy and corporate earnings. Now that we are pivoting back to more normal service spending, the normalization of spending habits was always going to manifest as a slowdown of economic growth. Not sure that is the worse thing in the world.

Naturally, the future is pretty uncertain, and things could slow more, become synchronized, or on the optimistic side, perhaps not much of a global slowdown at all. No denying our more forward-looking Market Cycle indicators are indicating a slowing environment. As evidence the slowing of economic activity is desynchronized, there remain a number of positive indicators in North America, while the global indicators are largely negative. We have seen some improvement on the global side but still early. Meanwhile, the fundamental data, which incorporates valuations (good) and earnings revisions (bad), have softened.

We do believe this bear market will manifest into the end of a market cycle that began way back in 2009. Given inflation is high, central banks have pivoted, and some sort of global recession/slowdown is in the cards, markets are resetting. Resetting isn’t enjoyable, but it does set the stage for the next bull cycle, which hopefully starts sooner rather than later.

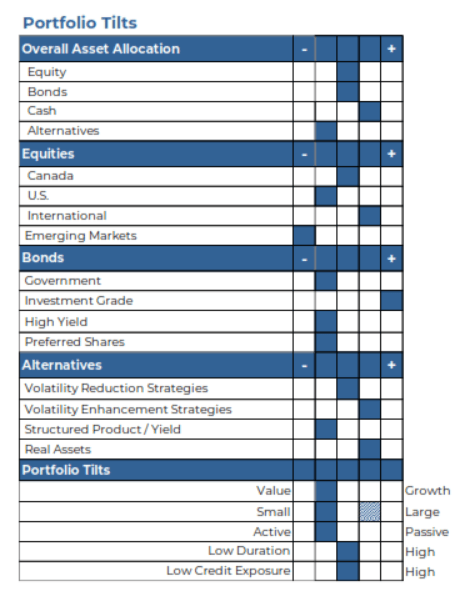

Portfolio Construction

No big changes to portfolio positioning this month. We remain market-weight equities given our split view that we could see a material market bounce just as much as we could see further weakness. Bonds remain a good allocation in this market, given higher yields, even if there is a bit more pain. The only minor change was our improving outlook for smaller-cap over larger-cap (from our last Ethos).

Erratic Thematics

Thematic ETFs and funds target stocks or investments positioned to benefit from potential shifts in technology, society, the environment, and demographics. Thematic investing has exploded in popularity over the last few years, driving investor demand to have focused exposure to one of the many game-changing industries. Many of these thematics also benefited in 2021 from the speculative market fever evident in the late stages of any bull cycle.

As the bull turned to a bear, this has put a hard stop to these thematic allocations. Reminding investors that even great long-term secular trends are not immune to the overall market cycle; investors have variable appetites for risk, interest rates, and the economy. Thematics have an incredible marketing strategy, stories sell, and I am sure you have never heard of a stock with a bad story, right? The same applies to thematic ETFs, but these stories can take decades to develop and can involve a very bumpy road along the way.

Perhaps at the start of 2022, you were sold a story on the future of mobility, specifically electric vehicles or self-driving cars. This story is very relatable, we continue to see more electric vehicles on the road every day, and the marketing for the industry is everywhere we look. The future of transportation will likely have a heavy tilt towards electric, but no one knows how long this will take to mature. We could be in the growth stage of the business cycle for decades. Sitting here 11 months later, the average drawdown on the future mobility category is -33.0%, and the position remains in your portfolio because why would you ever sell? You bought the position for the long term. Make no mistake, the story of the future is how this position got into the portfolio. And while we agree with the long-term secular change in the auto industry, the companies leveraged to this theme will follow a very volatile and often divergent relative path.

The future of the mobility theme is not alone. Inside the North American ETF landscape, there are currently about 97 thematic ETFs with greater than $100M in assets under management. Looking at the aggregate average performance year to date of the ETFs, it looks like it’s not that bad when compared with the All- Country World Index, with only an underperformance of about -6%.

When it comes to investing in thematic strategies, diversification is very important.

Using Thematic ETFs

A long-term secular trend is a powerful tailwind for an investment that has the right sail to catch the wind. But don’t gloss over due diligence because of a really compelling long-term story. Ask if you are getting in at a good time or a bad time. Always hard to tell, but if it has already doubled, concede that you missed that one for now. Plus, look at what is inside. Many of these strategies are very concentrated in a few names andnd understanding the underlying company’s exposure to the theme is important. Some are actively managed, while others rely on an index created to attempt to capture the theme. Either way,

don’t let the name of the strategy become a shortcut to due diligence.

Understand what is in it, it and bet you will be surprised on occasion.

Not all thematics will be successful. Some will fizzle out or amalgamate with other thematics. But some will be successful; therefore,

if you find an impulse to make an allocation in your portfolio, lean towards a diversified basket of thematics, the same way you would diversify your overall portfolio. Owning a basket of the above would have your portfolio down an average of -26% vs. simply holding a Cannabis ETF down - 51%.

We are not bearish on thematics. If anything, we would be more bullish at these prices. We simply believe that these future themes deserve more thought and attention when determining an allocation in portfolios. This next bull cycle will not be like the last one, which was underpinned by disinflation and low yields. Instead, expect inflation to be higher than what we are used to and yields to be relevant for portfolios again. In the next cycle, we expect that thematic investing will evolve alongside the overall investable universe.

— Craig Basinger is the Chief Market Strategist at Purpose Investments

— Brett Gustafson is a Portfolio Analyst at Purpose Investments

— Derek Benedet is a Portfolio Manager at Purpose Investments

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only. This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

Disclaimers

Echelon Wealth Partners Inc.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Inc. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional

advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.