For months now, the U.S. Federal Reserve has been hinting that the ‘taper’ of its quantitative easing (QE) program would begin, and last week the hints turned into an operation plan. Monthly bond-buying programs that are running at $120 billion per month will be reduced by $15 billion per month. The Bank of Japan has not been adding to their balance sheet for months now, and in October the Bank of Canada announced the end of its QE program. At the same time, forecasts for overnight interest rate hikes for most developed nations continue to be brought forward. The emerging markets have already started with nine countries having raised rates in the past three months. The monetary stimulus punchbowl hasn’t been pulled away yet, but it is being drained.

For markets, the Fed matters the most, so let us focus on them. Of course, this pending taper is bringing back memories of the taper tantrum of 2013. In 2013, Fed Chairman Bernanke began talking about tapering in May with the actual tapering of QE commencing in December. During the taper talk period, the U.S. 10-year yield rose quickly from 1.8% to 3.0%, the U.S. dollar declined, and the S&P 500 rose. After the taper started, yields fell back down, the dollar went flat, and of course the S&P 500 rose (is it just me or does that index always just go up?).

That was a fun trip down memory lane, now forget about it. We all like simple stories, neatly wrapped up with a bow. Fed does this, market reacts like that, simple. Unfortunately, looking at ONE tapering episode and drawing conclusions is not that simple. If n=1, good luck trying to reject the null hypothesis, for those statistical-oriented readers. Or if you prefer, its like apples and oranges.

The markets are certainly in a different place today compared with 2013. Bond yields aside, the S&P 500 was trading at 14x forward earnings in 2013 compared with 21x today. In 2013, the S&P 500 had just recovered to its previous high from 2007, which took about 5 ½ years. Today, the S&P 500 is 38% higher than its pre-Covid 2020 high (took six months). The U.S. economy was growing at an average of 2.5% in 2013, way lower than the trailing Q4 average of 4.9%. The trade-weighted U.S. dollar was low, by historical standards, around 82 compared with today’s 94.

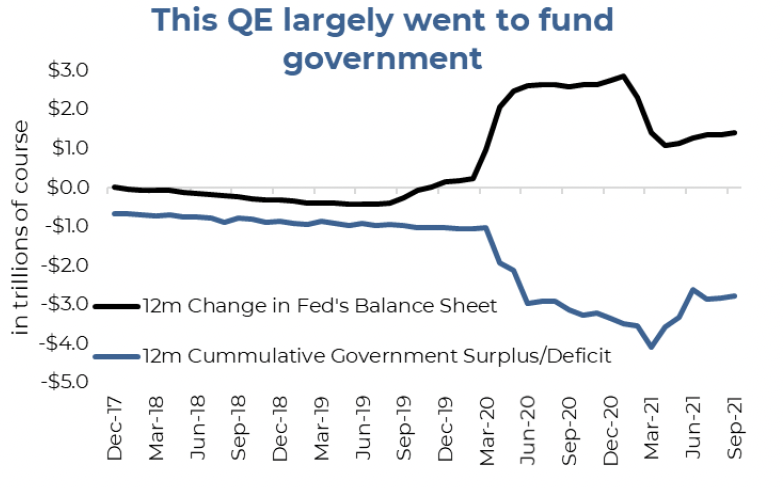

The biggest difference between these two tapers is where the money went and where it is going. The QE following the great financial crisis ended up more within bank balance sheets. Indirectly of course, but given banks reduced lending activities to repair balance sheets, the QE did not have a material economic impact since bank deleveraging was a natural counterbalance to QE. This time, QE has been funding government fiscal spending and support programs to help offset the impact of the pandemic. This QE had a central line right into the economy.

It is clear to see that as the government deficits come back down to earth, thanks to rising tax receipts as the economy recovers and emergency spending programs dwindling, there is less need for QE to fund the government. Demand (i.e., QE) is tapering at the same time supply (i.e., deficits) are falling. The good news is we are less likely to see bond yields rise because of this taper. The bad news is the Fed is able to taper because since fiscal spending is falling, there is a fiscal cliff on the spending side. Hopefully the economy has enough of its own momentum to get safely over this cliff.

Investment implications

The taper tantrum of 2013 does not provide a useful playbook for taper 2021. The market is in a different place, and the bond-buying programs ended up having vastly different impacts on the economy and markets. This makes it difficult to draw any hard conclusions.

The bigger stories for portfolios are that inflation continues to prove not so ‘transitory,’ short yields have risen, and the timing of rate hikes is approaching. In other words, the tightening cycle is almost upon us. Best to fill your cup from the punchbowl now.

Source: Charts are sourced to Bloomberg L.P. and Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used by Echelon Wealth Partners Inc. for information purposes only.

This report is authored by Craig Basinger, Chief Market Strategist, Purpose Investments Inc.

The contents of this publication were researched, written and produced by Purpose Investments Inc. and are used herein under a non-exclusive license by Echelon Wealth Partners Inc. (“Echelon”) for information purposes only. The statements and statistics contained herein are based on material believed to be reliable but there is no guarantee they are accurate or complete. Particular investments or trading strategies should be evaluated relative to each individual's objectives in consultation with their Echelon representative.

Echelon Wealth Partners Ltd.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Echelon Wealth Partners Ltd. or its affiliates. Assumptions, opinions and estimates constitute the author's judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them.

Purpose Investments Inc.

Purpose Investments Inc. is a registered securities entity. Commissions, trailing commissions, management fees and expenses all may be associated with investment funds. Please read the prospectus before investing. If the securities are purchased or sold on a stock exchange, you may pay more or receive less than the current net asset value. Investment funds are not guaranteed, their values change frequently and past performance may not be repeated.

Forward Looking Statements

Forward-looking statements are based on current expectations, estimates, forecasts and projections based on beliefs and assumptions made by author. These statements involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. Neither Purpose Investments nor Echelon Partners warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. These estimates and expectations involve risks and uncertainties and are not guarantees of future performance or results and no assurance can be given that these estimates and expectations will prove to have been correct, and actual outcomes and results may differ materially from what is expressed, implied or projected in such forward-looking statements. Unless required by applicable law, it is not undertaken, and specifically disclaimed, that there is any intention or obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice.

The particulars contained herein were obtained from sources which we believe are reliable, but are not guaranteed by us and may be incomplete. This is not an official publication or research report of either Echelon Partners or Purpose Investments, and this is not to be used as a solicitation in any jurisdiction.

This document is not for public distribution, is for informational purposes only, and is not being delivered to you in the context of an offering of any securities, nor is it a recommendation or solicitation to buy, hold or sell any security.